Personal loan serviceability is an assessment your lender makes to determine if you can afford the repayments on your new cash loan.

There are hidden elements to this calculation that can significantly affect the outcome, and it varies from lender to lender.

There are also responsible lending regulations that could see your expenses calculated at a much higher level than they actually are, to limit the risk of financial stress.

In this article, we will discuss the variables in the serviceability calculation that go beyond your own financial records, so you don’t get caught out before you apply.

How Lenders Calculate Personal Loan Serviceability

A serviceability calculation must determine if your income can comfortably cover loan repayments after all your living costs and existing debts are paid.

All three of these components have variables that can distort the outcome if they are poorly presented.

Income Calculation

Lenders need to consider both the amount you are earning, and the stability of that income.

This is easy for those with a full-time job and a set salary.

Where it gets complicated is when you also earn bonuses, over time, or work casual hours with variances in your take-home pay week to week.

Some lenders will consider 100% of your bonus income if you have earned it consistently for a period of time, whereas another may only count 50%.

Some lenders may use your lowest earning period as your baseline earnings for a casual employee, while some may use an average over a longer period.

This is why understanding a lender’s specific criteria is so important so you apply to the financier who will assess your income most favourably.

Expense Calculation

All applications will require an assessment of your expenses, and lenders take this very seriously.

Especially for fast cash loan products like a MACC loan.

When applying for a cash loan, you will almost always have to provide 90 days-worth of bank statements.

This allows the lender to securely analyse the data and calculate exactly what you are spending in that period.

You will still be required to estimate your living expenses, and both figures will be compared to a minimum living expense benchmark for someone in your demographic.

The higher of all three is most likely to be used in your assessment.

So, understating weekly costs rarely helps your application, but overstating them could unnecessarily hurt it.

Debt Repayments

If your existing debts have a fixed repayment amount, then this calculation is straightforward.

For those with credit cards, there will be more potential variation.

This is because your repayment is calculated as a percentage of your credit card limit, not the amount you currently owe.

The percentage can also vary between lenders, but is usually 3% to 4% of the total limit.

So even if you owe $0, your unused credit limit will reduce your capacity to service your new personal loan.

Cash Buffer

Most lenders will also add a buffer for what should be leftover in your budget after your personal loan repayments are factored in.

This varies depending on your circumstances and the lender’s risk profile, but it can be anywhere from $50 to $200+ a month.

If your cash surplus exceeds this amount, you pass this element of the credit assessment. If you do not have enough uncommitted income to cover the cash buffer, your application will likely be declined.

Once you consider all of this, it is clear that your serviceability is not the exact same thing as your personal budget.

Calculate Your Debt Service Ratio (DSR)

Some lenders will also calculate a DSR as part of their serviceability assessment.

This metric measures your total monthly debt commitments against your net monthly income, showing the percentage of your earnings that is already spoken for.

The formula is:

DSR (%) = (Total Monthly Debts ÷ Net Monthly Income) x 100

Here is a simple example for how to calculate a DSR:

- Net Monthly Income: $6,000

- Existing Debts: $900 (e.g., existing personal loans, credit cards, BNPL)

- Proposed Loan Repayment: $350

- Total Monthly Debt: $1,250 ($900 + $350)

Using the formula, the DSR is 20.8% ($1,250 ÷ $6,000 x 100).

While every lender has a different internal DSR cap, a lower number is always safer.

A higher ratio can signal financial over-commitment and potentially lead to your application being rejected.

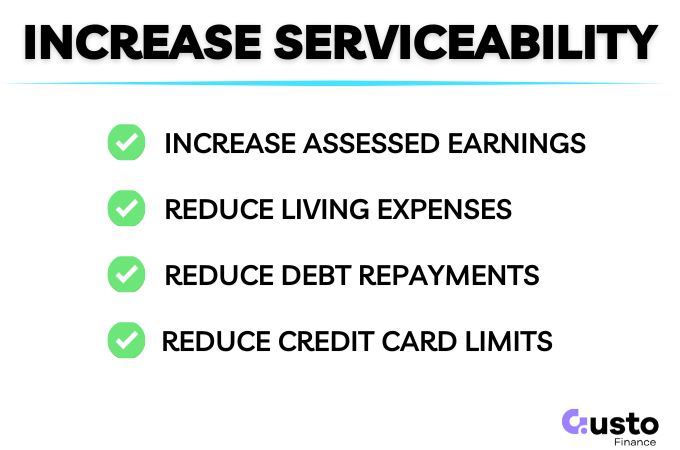

How to Improve Your Loan Serviceability

- Increase your included earnings. (e.g., transition to permanent work or provide longer histories of casual earnings).

- Reduce your living expenses prior to applying so your bank statements reflect lower spending.

- Reduce your debt repayments or lower the limits on your unused credit cards.

You can only cut your living expenses so far before you hit the benchmark expenditure floor.

Therefore, there is usually far more benefit to come from reducing your debt limits elsewhere or demonstrating consistent, stable earnings.

Frequently Asked Questions

Do unused credit cards affect loan serviceability?

Yes. Most lenders assess a potential monthly repayment based on your total credit card limit, not your current balance. Reducing the limits on cards you don’t need is a fast way to improve your serviceability.

What expenses do lenders look at for personal loan serviceability?

Lenders assess all your regular living costs via your 90-day bank statements. This includes rent or mortgage payments, existing loan repayments, groceries, utilities, transport, gambling transactions, and insurance.

I’m self-employed. How can I make my serviceability look clearer?

For a personal cash loan, the best practice is to keep your business and personal bank accounts strictly separate. When a lender assesses your 90-day statements, you want them to clearly see your regular personal income (your drawings/wage) and personal living expenses, without the confusion of business revenue and operational costs mixed in.

Ready to Assess Your Options?

If you are looking for a cash loan and want to ensure your application has the best chance of approval, the team at Gusto Cash is here to help.

We provide transparent, fast, and easy-to-understand MACC personal loans.

By understanding how serviceability works, you can get your bank statements and budget ready before you hit apply.