If you are receiving Centrelink income, you can get a personal loan depending on the type of benefit you receive and what portion of your total income it is.

There are strict credit criteria to satisfy, and your household budget must be watertight.

Most importantly, cash lenders like Gusto Cash have hard rules regarding the proportion of your income that comes from government benefits.

In this article, we will discuss the exact criteria you need to meet to get approved for a cash loan while on Centrelink, how to present your application, and the hard truths you must face if government benefits are your only source of cash.

The 50% Centrelink Income Rule

When assessing an application for a cash loan, Gusto Cash looks closely at the makeup of your income.

There are two high-level scenarios that are summarised in our Target Market Determination:

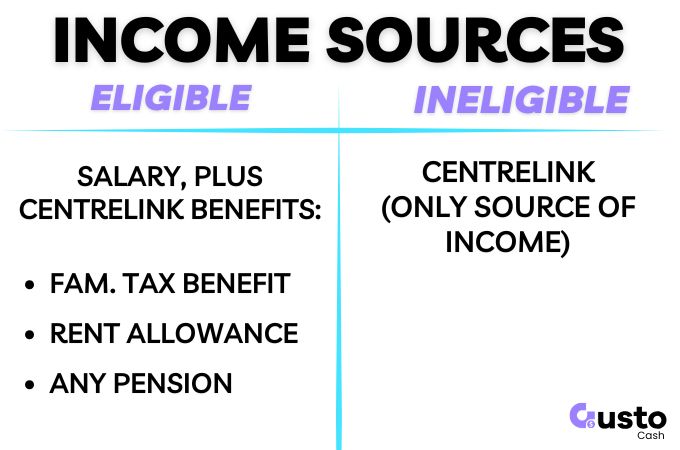

1. Centrelink as Your Sole Source of Income (Not Eligible)

If government payments are your only source of income, your borrowing power for a MACC loan with Gusto Cash is effectively zero.

While Centrelink provides a stable safety net, it is designed to cover essential living expenses, and may not have a sufficient surplus to service a new loan.

2. Centrelink as Additional/Supplementary Income (Eligible)

If you work and earn a wage, but also receive Centrelink benefits to supplement your household, your options increase significantly.

Many people work part-time or full-time and receive the Family Tax Benefit, Rent Assistance, or a flexible benefit that changes based on how many hours they work.

As long as your Centrelink benefits make up less than 50% of your total income you are eligible for a Gusto Cash loan (subject to other credit criteria).

Your working wage must be the primary source of money entering your bank account.

Example: If you receive $400 a week from Centrelink, you must earn at least $401 a week from your job to be considered for a loan.

Risks of Centrelink Being the Sole Source of Income

Lenders view stable employment as a strong sign that a borrower can meet repayment obligations.

Centrelink payments can be low relative to essential living expenses, and the amount leftover may be insufficient to service a MACC loan.

Benefit eligibility can also be subject to shifting government criteria, changes in your personal circumstances, or sudden cut-offs.

Therefore, some lenders consider them less reliable than a steady working wage when assessing your ability to repay a loan over a 12 to 24-month term.

By ensuring your primary income comes from employment, lenders protect both you and themselves from unmanageable debt.

Centrelink Income Categories and Cash Loans

Even if you meet the 50% rule, the type of Centrelink payment you receive still matters.

As a general guide, income categories are viewed as follows:

Acceptable (When combined with a primary wage):

- Family Tax Benefits (Part A & B)

- Rent Assistance

- Single Parenting Payments (if working part-time)

- Carer Allowance (if balancing work)

- Disability Support Pension (in some circumstances, if combined with allowable work limits)

Ineligible:

- JobSeeker (Newstart)

- Youth Allowance

- Austudy

How Centrelink Benefits Affect Your Borrowing Power

Your borrowing power is determined by how much disposable income you have after paying for your existing living expenses.

If you have a job, the extra money from acceptable Centrelink benefits will be added to your total income assessment.

This increases your potential borrowing power.

As long as you can demonstrate that both sources of income are sustainable and you have a healthy cash surplus each week, you will have a strong application.

Centrelink-Specific Alternatives

Centrelink Advance Payment

If you do not meet the 50% working income rule, or if you are in genuine financial hardship, you may be able to access a $500 advance from Centrelink.

This is then repaid over 13 fortnights and may be a more suitable alternative to a MACC loan for those on Centrelink benefits.

NILS

you may be able to access the No Interest Loan Scheme (NILS).

This is a community-based program that provides safe, zero-interest loans for essential goods and services to vulnerable Australians.

If you qualify, this is the safest and most affordable alternative to a traditional cash loan.

Frequently Asked Questions

What if I work part-time and receive the Single Parent Payment?

You can still apply for a Gusto Cash MACC loan, provided the income from your part-time job is greater than the amount you receive from your Single Parent Payment and any other combined Centrelink benefits.

Does the Family Tax Benefit count towards my total income?

Yes. When we calculate your borrowing capacity, we include your Family Tax Benefit as part of your total income. However, to pass the eligibility criteria, your working wage must still account for more than 50% of that total combined figure.

Why do lenders treat Centrelink income differently?

Lenders have an obligation to comply with responsible lending legislation. Relying entirely on a government safety net limits financial capacity to repay a loan, and increases the risk of financial hardship.

Can I get a loan if I am on JobSeeker but looking for full-time work?

No. JobSeeker is a temporary payment designed to support you while you find employment. Because it is temporary and not a primary working wage, it cannot be used to service a personal loan.

Apply for a Personal Loan Today

If Centrelink is your only source of income, we unfortunately cannot offer you a loan at Gusto Cash.

However, for those who are employed and simply use Centrelink benefits like the Family Tax Benefit or Rent Assistance to supplement their primary wage, you have excellent options available.

If you need between $2,001 and $5,000 and meet our income criteria, the team at Gusto Cash is ready to help.

Our online application is fast, transparent, and designed to provide you with the funds you need. Click below to get started.