Establishing a reliable track record of repayments when you owe money is a key foundation of the credit system in Australia.

This is why credit files exist, and one of the reasons why cash lenders will request to view your bank statements as part of their loan assessment.

If your transaction history shows a long list of dishonoured payments, you may have trouble obtaining a personal loan.

But will a missed repayment automatically make you ineligible for a cash loan? As is often the case in finance, the answer depends on a range of factors.

In this article, we will explain why all missed payments are not treated equally and what you can do to clean up your record prior to applying for a fast cash loan.

Understanding Payment Reversals

A payment reversal occurs when a direct debit payment is processed from your bank account and the funds in the account are insufficient to cover the payment.

Your account will briefly go into a negative balance before the payment is reversed. Often incurring a hefty dishonour fee from your bank.

This is not a good sign that you are managing your money effectively, and cash lenders will pay close attention to this.

But, not all reversals are the same.

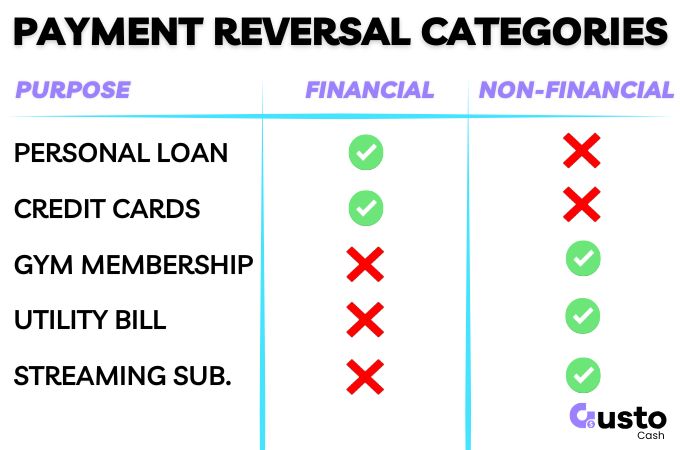

Financial vs. Non-Financial Reversals

The biggest differentiator is whether the payment reversal is related to credit or not. This is called a financial reversal.

While other missed payments still matter, a financial reversal may see you excluded from credit in the short term unless you take swift action.

Financial Reversals (Loans & Credit Cards)

A financial reversal is related to all types of credit. This could be a mortgage, personal loan, BNPL, or credit card repayment.

This is a major red flag for lenders for multiple reasons:

- You owe money and are not sticking to the repayment schedule.

- If you miss a payment, you will owe arrears payments in addition to your future scheduled repayments, placing additional pressure on your budget.

- Reversals may incur fees from both your bank and lender, amplifying the pressure on your budget.

This all adds up to you presenting as a higher risk than someone with zero reversals.

Non-Financial Reversals (Utilities & Subscriptions)

While it is still not a good sign that your last electricity or gym payment has reversed, it is not credit-related.

Lenders may be more forgiving of this depending on how often it has happened.

You may still have to explain why this occurred and potentially show proof that a large balance is not owed on the account.

Consequences of a Payment Reversal

The consequences of a payment reversal will mostly depend on what you do next.

Your highest priority should be making up the missed payment as quickly as possible. The longer you leave it, the more severe the consequences become.

Impact on Loan Eligibility

If you have a financial reversal and are currently in arrears on an existing loan, you will generally not be eligible to apply for further credit.

Your cash loan application will be flat-out rejected by most lenders if you have a current arrears balance.

So pay that first, no matter what!

Once you have corrected the issue, there are lenders who will consider your application, but your options will be fewer than someone with an exemplary credit profile.

Credit File Impact

There are two credit systems currently operating in Australia: Comprehensive Credit Reporting (CCR) and negative credit reporting.

- Comprehensive: Includes the status of current loans and whether you are up to date or behind in repayments, plus all associated negative credit reporting instances.

- Negative: Only records significant events like formal payment defaults, court judgments, and insolvencies.

This is important to know because if you miss a payment, the clock is ticking to correct this before it appears on a comprehensive credit report.

Lenders have a small window of tolerance where you can repay this with no mark appearing on your comprehensive credit file (but it’s not long!).

Banking Transaction History

When applying for a MACC personal loan, lenders will almost certainly require 90 days’ worth of bank statements to assess your income and living expenses.

Because of this, payment reversals will be easily detectable, even if they never made it onto your formal credit file.

The good news is, a messy bank statement is often easier to fix with a little patience.

What to Do If I Miss a Payment and Need a Cash Loan

Not all hope is lost if you miss a repayment while also planning to apply for a new personal loan.

You will still have options if you take the following steps:

1. Contact Your Lender Immediately

As soon as you notice the reversal, call the company you owe money to.

Notify them that you are aware of the reversal and will be taking steps to correct it.

Clarify the grace period before it shows up on your credit file.

2. Pay the Arrears Balance

Make the payment as soon as you can and provide a record of the payment to your lender.

This is important just in case there is an administrative error and your credit file is affected.

How Many Reversed Payments Will Ruin My Application?

With some lenders, your application will be heavily affected by a single payment reversal.

Other lenders will tolerate a limited number, depending on the factors we have discussed.

As a general rule of thumb, every reversal will be scrutinised and is going to reduce your options.

If you have five or more payment reversals on your recent bank statements, you are less likely to be approved for a loan.

This threshold may be even smaller if they are financial reversals.

At Gusto Cash, approval is dependent on your overall financial health.

What If I Have Damaged My Credit File?

If you have missed the above steps due to tougher circumstances or past mistakes, not all hope is lost.

Your options will be limited, and you may need to look at bad credit or second-chance personal loans.

Gusto Cash considers your situation beyond just your credit file. Any additional blemishes on your bank statements will need to be understood prior to a decision being made.

What matters most in these circumstances is your more recent financial record.

If you can demonstrate the following, you will have a much stronger chance of being approved:

- All existing loan arrears have been paid, or on a payment plan.

- You have control of your expenses and can evidence enough disposable income to support the new loan.

- You have not recently been applying for multiple payday loans (SACCs) or excessive wage advance products.

Why Lenders Must Decline Potential Hardship Cases

Lenders don’t just decline applications because they want to avoid risk; there are strict legal regulations they must comply with when lending money.

Under the National Consumer Credit Protection Act, lenders are obligated by law not to lend to anyone who may be at risk of “substantial hardship”.

If you are regularly failing to meet your existing financial obligations (evidenced by frequent payment reversals), the risk of hardship is high.

Therefore, approving a loan could be a breach of responsible lending laws.

Cleaning Up Your Bank Statements

A cash lender is generally only going to look at your last 90 days of bank statements.

So, if you had a bad week that was a one-off event, there may be no long-term consequences as long as you can provide a reasonable explanation.

If you quickly make up all repayments and ensure there are no further reversals, after 90 days, your bank statement will be looking fresh and squeaky clean!

Frequently Asked Questions

Will one dishonoured payment ruin my personal loan application?

Not necessarily. While a single reversal isn’t ideal, but some lenders consider a broader look at your financial behaviour over a 90-day period. If it was a rare, one-off mistake, and you quickly rectified it, it is less likely to result in an automatic decline.

How far back do lenders look in my bank statements for reversals?

When assessing an application for a MACC personal loan, lenders will typically securely consider your last 90 days of bank transactions.

Can I apply for a cash loan if my bank account is currently in the negative?

This depends on the reason it is in a negative balance, the frequency with which this may have happened in the past, and your overall capacity to service the additional loan repayment. Lenders must abide by responsible lending laws and cannot provide a loan that will put you into further financial hardship so affordability is critical.

Does a payment reversal automatically go on my credit file?

No, a bank dishonour or payment reversal doesn’t hit your credit report immediately. However, if the reversed payment was for an existing credit product and remains unpaid past the lender’s grace period (typically around 14 days), it can be reported as a late payment under your Comprehensive Credit Reporting (CCR) history.

Preparing for Your Personal Loan Application

Payment reversals are a strong warning that someone’s financial health is at risk, and a lender will look very closely at every instance when you apply for a cash loan.

However, you always have options.

By addressing arrears immediately and seeking guidance, you can still find a path to approval.

If your recent history is too messy, you can rectify the situation in less than 90 days and reapply with much more confidence.

If you’re unsure where you stand, reach out to the team at Gusto Cash today.

We offer transparent MACC personal loans and can help you understand your eligibility in minutes.