Small Amount Credit Contracts (SACCs) are a type of lending product that was born out of legislation banning traditional payday loans.

However, most lenders still view these products as payday loans even if they have a new legal name.

Frequent use of these products will heighten your risk profile in the eyes of a lender when you are applying for a larger Medium Amount Credit Contract (MACC) personal loan.

In this article, we’ll discuss the true impact of SACC loans on your credit file and how to prepare for a successful personal loan application in the future.

Understanding SACCs: The New Payday Loan

Traditional Payday Loans

Pre-2013, a payday loan was typically a small unsecured loan to be repaid within a short period of time (usually a week or two).

In return, the lender would charge a very high fee or interest rate (often well over 100% if annualised).

These charges were uncapped, and the excessive costs often led to people needing to borrow again just to repay the original loan, trapping them in an endless debt cycle.

New Payday Loans (SACCs)

The SACC legislation was introduced to provide guardrails for lenders so that repayment structures and fees were fairer.

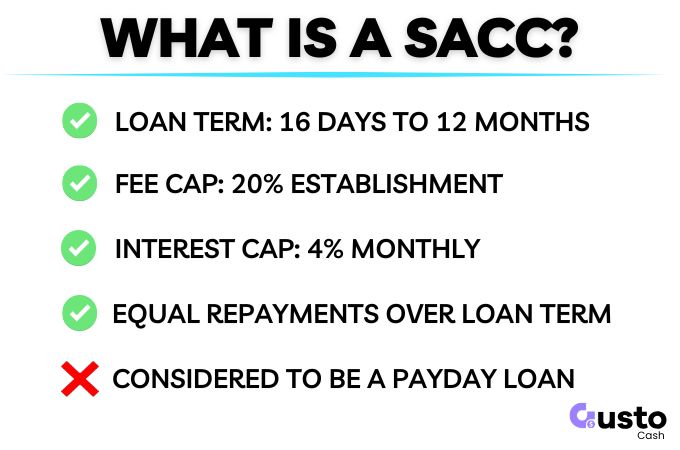

A SACC is strictly for loans under $2,000.

While safer, they are still expensive loans even with the current fee caps in place:

- 20% establishment fee.

- 4% monthly fee based on the borrowed amount.

A SACC loan must also have a repayment term between 16 days and 12 months. While this is a better outcome for consumers, it is still an expensive product to engage with.

Frequent use of these loans is a strong indicator that your household budget is under pressure.

Why Borrowers Turn to Short Term Cash Lending

People turn to payday loans to fill the need for urgent cash, often in response to unexpected bills like car repairs or medical expenses.

They can be a useful tool for those who have had credit problems in the past and cannot access traditional credit.

However, a MACC personal loan (offered by Gusto Cash) is generally a more cost-effective way to access urgent cash relative to the amount borrowed.

The establishment fee is capped at $400 and you only pay interest on the reducing balance as you repay the loan.

Relying on the smaller, more expensive SACC loans regularly is a red flag that lenders will pay attention to when assessing you for any other type of personal loan.

How SACCs Affect Your Credit

Every time you apply for a SACC loan, there is a mark left on your credit file that will be visible to other lenders.

This will be evident regardless of whether you are approved or not.

Each lender has a different policy on how this affects your loan eligibility.

Some lenders will overlook past SACC borrowing if no new applications have been made in over 6 to 12 months.

Others will tolerate a limited number of SACC applications in the past 90 days.

There are also Australian regulations that deem a borrower unsuitable for another SACC if they have had two or more in the past 90 days.

So if you are applying for another SACC loan after you hit this threshold you are ineligible by law.

While MACC lenders are not bound by that same 90-day SACC rule, they still view heavy recent usage as a risk factor that will be considered in the assessment.

Why Lenders Decline Applicants with Excess SACC Use

Lenders will scrutinise your credit history and 90 days of bank statements as part of the application process to assess your spending habits.

Lenders are obligated by law not to lend to anyone who may be at risk of substantial hardship.

Loan Serviceability (Can You Afford It?)

The high fees associated with a SACC loan require substantial repayments. If you do not have sufficient income to support these existing SACC repayments AND the new MACC personal loan you are applying for, a lender cannot legally approve your loan.

Loan Eligibility (Are You Too Risky?)

Most lenders have hard rules on the regular use of payday lending products. If you have a clear pattern of dependency, you may be deemed ineligible for a MACC loan before your affordability is even fully calculated.

If I Have Used SACC Loans, What Now?

If you’ve used payday loans recently you may still be eligible for a personal loan, but it depends on the rest of your risk profile and financial situation.

As long as you can demonstrate that you can comfortably afford the repayments on an additional loan then you may be eligible sooner than you think.

However, heavier use of payday loans may prevent you from getting additional finance until you can improve your budget management and financial discipline.

How to Strengthen Your Loan Application

If you have been a heavy user of SACC products, you may need to stop for a reasonable amount of time prior to seeking a larger loan.

If this is too difficult to do from a budget point of view, you may not be ready for additional credit.

Avoid Substitute Forms of Credit

There are other products available that may seem harmless but create a similar problem for your creditworthiness.

Frequent use of Wage Advance apps or heavy reliance on Buy Now, Pay Later (BNPL) services can also be sticking points in a personal loan application.

Common Payday Loan Mistakes to Avoid

- Using SACC Loans as a Quick Fix Too Often: Relying on them to cover regular living expenses can trap you in a cycle of dependency.

- Not Planning for Annual Expenses: Keep a written record of infrequent bills (rego, insurance) and set up an automatic transfer into a separate savings account each pay cycle.

- Ignoring Emergency Savings: Even putting away $10 or $20 a week can save you from needing an expensive short-term loan when a minor emergency hits.

Frequently Asked Questions

What is the difference between a SACC and a MACC?

A SACC (Small Amount Credit Contract) is for loans up to $2,000 and carries a 20% establishment fee and 4% monthly fee. A MACC (Medium Amount Credit Contract) is for loans between $2,001 and $5,000, typically featuring a capped $400 establishment fee and an annual interest rate up to 48%, making it generally cheaper relative to the amount borrowed.

Will Gusto Cash approve my loan if I have an active SACC?

It depends on your overall financial health and serviceability. If your income can comfortably cover your living expenses, the active SACC repayments, and the proposed MACC loan repayments without causing financial hardship, you may still be considered.

Why are Wage Advance apps treated like payday loans?

While wage advance apps often don’t charge traditional interest, lenders view them similarly to SACCs because frequent use indicates that your standard income is not stretching far enough to cover your daily living expenses between pay cycles.

How long should I wait to apply for a MACC after paying off a payday loan?

You don’t need to wait if you can comfortably afford the repaymnts of your MACC loan. Because cash lenders typically review your last 90 days of bank statements, waiting 90 days after your final SACC payment will ensure your transaction history is completely clear of high-cost short-term credit, greatly improving your chances of approval.

Can I Get a Personal Loan After a Payday Loan?

Payday loans can be a helpful tool of last resort to deal with a one-off emergency.

However, if you are relying on these services just to get by, it is a symptom of a greater issue.

Occasional past use may limit your options, but you may still be able to secure a MACC loan if placed with the right lender. Get in touch with the team at Gusto Cash below to see if you qualify today.