If you have previously defaulted on a payment obligation, your credit file could be marked with a default listing.

This will hurt your credit score and place you in a higher risk category for the duration of the default period.

But did you know that a lender can also see the current status of that default?

If you have taken steps to pay it, this is a massive step toward lowering your risk profile in the eyes of a lender.

In this article, we will discuss the different categories of default, how they will be treated by a potential cash loan lender, and what you can do to get approved.

What is an Unpaid Default?

An unpaid default is a formal record listed on your credit file that indicates you have not met your repayment obligations on a loan, bill, or other contractual agreement.

Most people are familiar with a financial default, where you have fallen behind on payments due for a loan or credit card.

However, many are not aware that you can also be defaulted when you fall into severe arrears on your power bill, phone bill, or other services.

If you are applying for a personal loan with unpaid defaults, the type of default will be treated very differently by a lender.

Financial Defaults (e.g., Loans & Credit Cards)

A financial default effectively tells the lender that you have borrowed money in the past and not repaid it as per your loan agreement.

Personal loans, payday loans (SACCs), credit cards, and mortgages all fall under the category of a financial default.

This is a massive red flag. It can be extremely challenging to be approved for a new cash loan when you have an unpaid financial default hanging over your head.

Utility Defaults (e.g., Phones & Power Bills)

Some cash lenders will be more lenient if the default is for a utility or an unpaid service (like a gym membership or telco contract).

It is still an indicator that you may be at higher risk than the average borrower, but fewer lenders will outright reject you based on a utility default alone, assuming your recent banking conduct is clean.

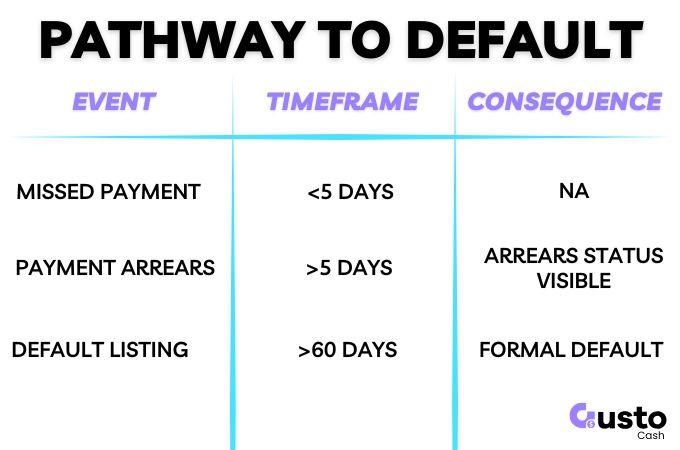

Events That Lead to a Payment Default

Defaults do not happen overnight. There is a specific timeline of events that leads to a black mark on your credit file.

1. Missed Payment

If you have missed a payment by a few days, this is only a minor hiccup. As long as you take rapid action to correct the problem, there will be no long-term consequences.

However, if you remain in arrears for longer than 14 days, it may become visible to other lenders via your credit report.

2. Payment Arrears

If you fall into arrears against your repayment schedule, this will become visible on some versions of your credit file.

An increasing number of lenders in Australia now participate in Comprehensive Credit Reporting (CCR), which includes a monthly status of your outstanding loans.

If you are in arrears, it will show this for the length of time you are behind. The faster you correct the problem, the better.

3. Payment Default Listing

A lender will only list a formal default on your credit file after they have gone through a lengthy process to resolve the situation.

This is likely to include:

- Multiple notices that you have missed a payment and are in arrears.

- Multiple attempts to make contact with you via phone, SMS, email, and post.

- A formal notice of default warning you of the impending action.

By the time you are defaulted, you have had fair warning.

If you then repay the debt, your default listing will be updated to reflect a Paid status. If you have not paid the debt, it remains an Unpaid default.

How Long Do Defaults Stay on Your Credit File?

A default will remain on your credit report for five years.

However, the status of the default will be updated when it changes. It is vital for your future financial prospects that the status is updated to Paid as soon as possible.

Lenders take this into account; it shows that while you may have struggled, you eventually did the right thing and cleared your debt.

Paid vs Unpaid Defaults

Any risk assessment that a lender completes is a spectrum. However, some factors lead to an instant decline.

In the case of financial defaults, the vast majority of mainstream personal loan providers will not consider an application where there are unpaid financial defaults.

The good news is that if you can show you have repaid the outstanding loan in full, you can apply for a cash loan immediately.

The damage to your credit score is done, and you will likely be limited to a second chance loan, but approval is absolutely possible.

Why Some Lenders Are More Flexible Than Others

Many traditional banks rely solely on credit scores to automate their approvals. If your score is low due to a default, the computer says no.

However, non-bank cash lenders (like those offering MACC personal loans) have business models designed to look past historical credit mistakes.

They do this by looking at your current financial behaviour.

Most of these lenders will securely scrape 90 days of your bank statements as part of the loan application.

Every transaction will be analysed to identify your current level of financial responsibility.

If your bank statements show consistent income, no recent dishonour fees, and a healthy cash surplus, a specialist lender is far more likely to overlook a 3-year-old paid default.

Frequently Asked Questions

Will Gusto Cash approve me if I have a default?

Yes, but it depends on the remaining balance outstanding, plus the type and status of the default. If you have an unpaid financial default, this does more harm to your application but is not an immediate dealbreaker. However, if the default is fully paid, or if it is a minor utility default and your recent 90-day bank statements are completely clean, approval is more likely (subject to all credit criteria).

How do I check if I have a default on my file?

You are entitled to a free copy of your credit report every few months from major credit bureaus in Australia, such as Equifax, Experian, or Illion. You can request your report online to check for any active defaults.

Does a paid default get removed from my credit file?

No. Paying a default does not remove the listing from your credit file; it will still remain there for the full five years. However, its status will change from Unpaid to Paid, which makes you significantly more attractive to future lenders.

Only Apply Once You Understand Your Defaults

While you should always try to meet your repayment obligations before taking on additional debt, circumstances may dictate that you need cash now for an emergency.

Not all unpaid defaults will be treated equally by a potential lender, and the type of default will heavily determine your current eligibility.

If you have financial defaults preventing you from being approved for a personal loan, you now know to prioritise the repayment of these debts so you have options sooner.

If your past defaults are paid and your current bank statements are looking healthy, the team at Gusto Cash is ready to help.

We look at the bigger picture to find a MACC loan solution that works for you today, regardless of your past.