Buying a house requires most people to take on the largest debt they will ever have to repay. It also requires lots of saving and disciplined budgeting just to get approved!

Once that is taken care of, you technically have the freedom to take on additional smaller loans without the fear of it impacting your home ownership.

But will you be approved for a cash loan after taking out a mortgage? The short answer is yes, as long as you can afford the additional repayments.

In this article, we will discuss the timing of your personal loan application, whether you are better off borrowing within your mortgage, and the optimal strategy to save you the most money.

Timing Your Loan Application After Buying a House

Considering you will be paying your mortgage for 30 years, there is a lot of time after buying a house where your finances will be affected.

Leading up to that point there are timeframes where any additional finance could be detrimental to the property purchase process.

Risks of Applying Before Settlement

Once you sign an unconditional contract of sale on a property, you still have 5 to 6 weeks until the settlement date in most cases.

The big risk here is that you do something that could prevent your mortgage from settling on time.

If your bank conducts a final credit check and sees you have just taken out a new personal loan, it alters the debt-to-income ratio they originally approved.

Even if your need for cash is a genuine emergency, you must delay until after your settlement or you risk derailing the whole thing.

This could lead to penalties, including forfeiting your deposit if your finance is pulled and you cannot proceed with the purchase.

So err on the side of caution always.

Applying After Mortgage Settlement

Once your mortgage is officially settled, there is nothing holding you back and you can focus on finding the right loan for you.

You can now make a fresh assessment of your finances and how much debt you are comfortable taking on to cover unexpected expenses like furniture, moving costs, or renovations.

How a Mortgage Affects Your Personal Loan Eligibility

Your eligibility for a cash loan will be impacted by the same standard variables (credit history, employment stability, etc.) as your mortgage application.

The only difference is that you now have mortgage payments to include in your household budget.

When applying for a cash loan, the lender will require 90 days of your bank statements to verify that you are comfortably managing your new mortgage payments.

Borrowing Power and Disposable Income

The amount of disposable income you have after paying your mortgage and other living expenses will determine your borrowing limit for a cash loan.

Some people find themselves house poor in the first couple of years, allocating a massive portion of their income to mortgage payments.

If your bank statements show you are living paycheck-to-paycheck, a cash lender cannot legally approve a new loan due to responsible lending laws.

However, if you have borrowed well within your means for your mortgage and have a healthy cash surplus each month, this will not be an issue.

Does a Mortgage Improve My Credit Profile?

The final influence on your personal loan eligibility is how a cash lender will treat your new situation.

Every lender has different rules for how they assess risk.

Most cash lenders view your new asset position (you are a property owner!) as a positive.

It shows stability and a track record of responsible financial management.

Rarely will owning a home harm your eligibility for a cash loan, provided your serviceability math checks out.

Should I Just Increase My Mortgage Instead?

If you need $4,000 for unexpected home repairs or new furniture, you may prefer to just increase (top-up) your home loan.

The interest rate on a mortgage is much cheaper than a personal loan, and the monthly repayments will be tiny.

But will this actually save you money?

Because a mortgage is stretched over decades, the answer is often no unless you pay much more than the minimum.

Banks love it when you add small expenses to your mortgage because they collect interest on it for 30 years!

Cost Comparison: Mortgage Top-Up vs. MACC Personal Loan

Let’s assume you have a $4,000 emergency expense.

Scenario 1: Increase Your Mortgage

- Amount: $4,000

- Interest rate: 6% p.a.

- Repayment term: 30 years

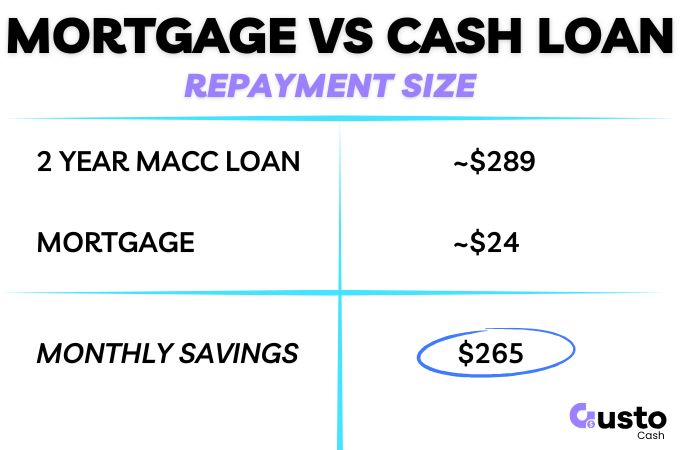

- Monthly repayment: ~$24

- Total interest payable: ~$4,633

Due to the massive 30-year repayment period, you end up repaying over $4,600 in interest on top of the original $4,000 borrowed.

Your $4,000 expense ends up costing you over $8,600, and you will be paying it off long after the furniture has been thrown out.

Scenario 2: Separate MACC Personal Loan

- Loan Amount: $4,400 ($4,000 cash + a standard $400 establishment fee)

- Interest rate: 48% p.a. (MACC maximum)

- Repayment term: 2 years (24 months)

- Monthly repayment: ~$289

- Total interest payable: ~$2,536

This is a much more aggressive repayment schedule. However, the total cost savings are significant even though the interest rate is much higher.

The total amount repaid is roughly $6,936.

Despite the higher upfront fee and higher interest rate, the aggressive 2-year term makes this option over $1,600 cheaper than burying the debt in your 30-year mortgage!

The Cheapest Strategy (Scenario 3)

For the more disciplined borrower, there is a third option.

What if you top up the mortgage at 6%, but voluntarily make the aggressive $289 monthly repayments of a personal loan?

You would pay off the $4,000 in just over a year and pay barely $150 in total interest.

The real question is: will you stay disciplined and make the higher repayments if you are not legally required to?

If the answer is no, a separate personal loan forces you to pay the debt off quickly.

Summary Table

| Feature / Metric | Scenario 1: Increase Mortgage (30 Years) | Scenario 2: MACC Loan (2 Years) | Scenario 3: Mortgage Top-Up + Aggressive Paydown (~1.2 Years) |

| Base Amount Borrowed | $4,000 | $4,000 | $4,000 |

| Upfront Fees | $0 (or rolled in) | $400 (Establishment Fee) | $0 (or rolled in) |

| Total Loan Principal | $4,000 | $4,400 | $4,000 |

| Interest Rate | 6.00% p.a. | 48.00% p.a. | 6.00% p.a. |

| Repayment Term | 30 Years (360 months) | 2 Years (24 months) | ~14 Months (Paydown) |

| Monthly Repayment Size | ~$24 | ~$289 | ~$289 |

| Total Interest Charged | ~$4,633 | ~$2,536 | ~$150 |

| Total Out-of-Pocket Cost | $8,633 | $6,936 | $4,150 |

| Financial Discipline Required | Low: Set and forget, but pay for decades. | Medium: Mandatory structure forces quick payoff. | Very High: Relies entirely on your willpower to pay extra. |

Frequently Asked Questions

Will applying for a personal loan impact my ability to refinance my mortgage later?

A MACC personal loan is a short-term commitment (maximum 24 months). If you plan to refinance your mortgage three years from now, your personal loan will already be fully repaid and closed, leaving your borrowing power completely unaffected.

Do I have to use my house as security for a Gusto Cash loan?

No. MACC personal loans provided by Gusto Cash are entirely unsecured. We will never take your newly purchased home (or any other asset) as collateral for a loan.

How soon after settlement can I apply for a cash loan?

You can apply the very next day if needed. However, you have an obligation to be transparent in your original mortgage application and this should only be a response to a genuine change in your circumstances.

Structuring Your Loan for Success

Once your home loan has settled, you can apply for a personal cash loan without risking your property purchase.

You now have major assets in your name and a track record of responsible saving.

The real question is how you should structure that loan to get the best financial outcome.

Hiding short-term debts inside a 30-year mortgage might feel cheaper month-to-month, but it will cost you thousands more in the long run.

If you are ready to tackle your post-settlement expenses head-on with a quick cash loan between $2,001 and $5,000, the team at Gusto Cash is ready to help!