If you have missed a repayment on an existing loan or credit card, you usually have a small window of time to make this up before it becomes visible on your credit file.

As long as you catch up within 14 days, no long-term harm is done to your credit score.

Beyond this, there are various levels of credit events that can be reported, which can severely impact your ability to get a personal loan in the future.

In this article, we will discuss exactly how and when a late payment is reported to a credit bureau and the typical timelines involved.

Credit Reporting Agencies in Australia

There are three primary credit reporting agencies in Australia: Equifax, Experian, and illion.

Each compiles your credit data independently, and different lenders may report to one, two, or all three.

To complicate things further, there are two different reporting systems operating in Australia:

Negative Credit Reporting

This is the legacy credit reporting system. Under this older framework, a standard 15-day late payment goes completely under the radar.

The credit information provided is strictly limited to:

- Credit enquiries (the date and amount you applied for).

- Significant negative credit events such as formal default listings, court judgments, and bankruptcies.

Comprehensive Credit Reporting (CCR)

The modern CCR system includes all the negative data mentioned above, plus periodic reporting on the current status of all your open loans.

Because of CCR, an account in arrears is highly visible on your credit file almost immediately after the 14-day grace period expires.

To summarise the additional data visible under CCR:

- The current status of all open loans (whether they are up to date or in arrears).

- Advere events such as default, court judgments, or insolvency.

- If a Hardship arrangement has been implemented (this remains visible for 12 months).

The vast majority of mainstream personal lenders utilise the CCR system to make responsible lending decisions.

However, there is no obligation to use CCR and plenty of lenders still use negative credit reporting.

Especially in short term cash lending.

Timeline of a Late Payment

Under the modern CCR system, your payment history is constantly being updated.

How Long Before a Missed Payment is Reported?

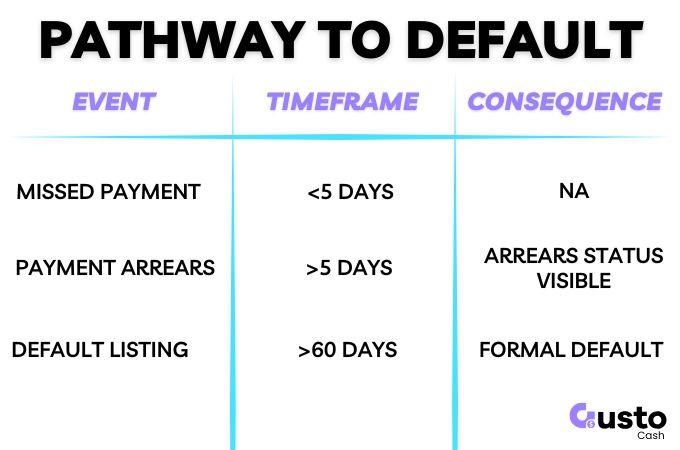

The credit bureaus have a built-in grace period of exactly 14 days before a missed payment can be recorded on your credit file as a Late Payment.

If you catch up on the payment before that 14-day window closes, you are generally in the clear.

When Lenders Notify Credit Reporting Agencies

Lenders typically send updated credit data to the bureaus once a month.

If your payment was late but you caught up quickly, there’s a strong chance it won’t be reported at all.

However, if it remains overdue into the lender’s next reporting cycle, the credit bureau will be notified.

Once reported, the missed payment will be evident on your credit file for the next 24 months, and your credit score will take a hit.

How Lenders Treat Different Levels of Late Payments

When applying for a personal loan, the lender will assess the severity of your missed payments.

One-Off Missed Payment

If you have missed one payment in the last two years but corrected the issue quickly, the impact is usually minimal.

This is lender dependent and some major bank and credit unions may exclude you on this alone.

You should retain access to plenty of non-bank lenders that have some more flexibility in their credit policy.

Multiple Missed Payments

Once a pattern emerges of regular missed payments, your choices will become far more restrictive.

A lender will see this as a sign of budget stress.

Furthermore, cash lenders almost always require 90 days of bank statements to assess your application.

Even if a missed payment hasn’t hit your formal credit file yet, the lender will see the payment reversals and dishonour fees in your bank transaction history.

Any sign that you are currently struggling with existing debts will lead to an automatic decline under responsible lending laws.

What is the Difference Between a Late Payment and a Default?

A default listing is a much more serious mark on your credit file with longer-lasting consequences.

If your late payments are left outstanding, a formal default can occur after 60 days or more.

Your lender must make genuine attempts to contact you to resolve the problem and must send written notices of their intention to list a default.

They must give you at least 30 days to rectify the issue before hitting the default button.

The Consequences of a Default

It will be more difficult for you to access mainstream credit while you have one of these negative events listed on your credit file.

- A late payment stays on your file for 2 years.

- A default will stay on your file for 5 years.

Your credit score will take a hit, which can heavily limit your access to future personal loans or restrict you to higher-cost, bad-credit lending options.

However, once you pay a defaulted debt, the status of the default will be updated to Paid, but the mark will still remain.

This small improvement can help you access more non-bank lenders and over time you credit score will improve if you ensure all loan payments are kept up to date.

Some lenders may consider eligibility while you have unpaid defaults, but will be subject to strict criteria.

Frequently Asked Questions

Can I get a loan with Gusto Cash if I have a late payment on my file?

We assess every application on its individual merits. If you have a single, isolated late payment from a year ago but your current 90-day bank statements show a strong, positive balance and consistent income, you still have a higher chance of approval.

How do I fix a late payment listing?

You can only challenge a late payment listing if there has been a genuine administrative error. You can dispute this directly with the credit provider, who would update the bureau if resolved in your favour. If the late payment was genuinely your fault, it cannot be removed and must age off your file over two years.

If I pay off my late payment, does my credit score immediately go back up?

No, your credit score will take some time to recover. While bringing your account up to date is important to prevent the debt from escalating into a formal default, the record of that specific late payment will still remain on your credit file for up to 24 months. Your score will gradually recover as you demonstrate a new, consistent track record of on-time payments.

Do late payments on utility or phone bills show up under the 14-day rule?

No. The 14-day Comprehensive Credit Reporting (CCR) rule generally only applies to licensed credit products like personal loans, credit cards, and mortgages. And only from lenders who participate in CCR. Utility providers and telcos do not participate in this standard monthly reporting. However, if you leave a utility bill unpaid for an extended period (usually 60 days or more) they can list a formal default on your credit file, which will impact your score for 5 years.

Protect Your Credit Report

Lenders like to see a history of prudent management of your finances.

If you miss a payment, it is your responsibility to correct the issue as quickly as you can to beat that 14-day buzzer.

Prevention is much easier than the cure.

Check your bank statements regularly, set up calendar reminders for your direct debits, and ensure you have a small cash buffer in your account to prevent accidental dishonours.

If your recent banking history is looking healthy and you need a cash loan between $2,001 and $5,000, the team at Gusto Cash is ready to provide a fast, fair, and transparent assessment.