While a cash loans is often a short-to-medium-term financial commitment, it is still common for a borrower’s circumstances to change before the debt is fully repaid.

If an emergency hits and you need to borrow a little extra, or if your budget tightens and you need to lower your monthly repayments, you might consider refinancing.

But do you have to go through the hassle of finding a brand-new lender?

The answer is no.

Refinancing a cash loan with your current lender is a very common scenario.

In this article, we’ll discuss how an internal refinance works, why it is so common in the Medium Amount Credit Contract (MACC) space, and how to determine if it is the right choice for you.

Internal vs. External Refinancing

Cash loan refinancing is the process of replacing an existing loan contract with a new one.

Usually to access additional funds, or reduce your loan repayments by extending the repayment term.

You can do this internally (with the same lender) or externally (to another lender).

Internal Refinance

You apply to restructure your debt with your existing lender. The lender closes your current contract and immediately opens a new one for you.

This is much more common in cash lending because the process is often faster if you have established a track record of reliable repayments over time.

External Refinance

You apply with a completely different lender.

The new lender pays off your old debt, closes that account, and you start fresh with them.

Will My Current Lender Approve a Refinance?

You can usually refinance a personal loan with the same lender if you still meet their required lending criteria.

Lenders like Gusto Cash value good customers. If you have a strong track record of making your payments on time, keeping you as a customer is beneficial to the lender.

However, you are still going to have to pass a standard credit assessment on the day of your new application.

What Lenders Check in a Refinance Application

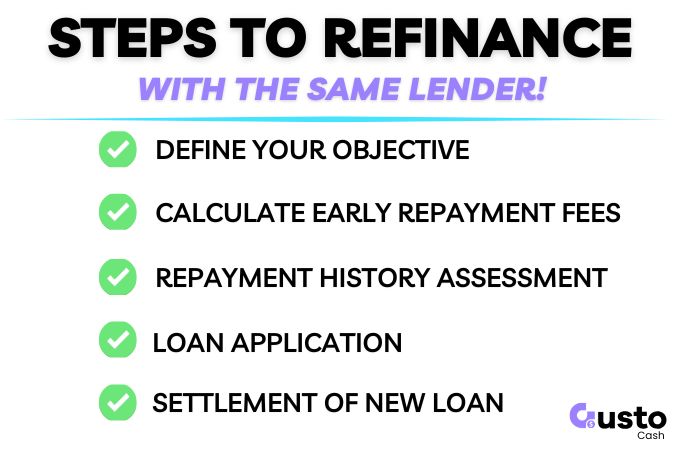

1. Repayment History

The biggest advantage you have is that the lender already knows how you manage debt and have a record of your repayment history.

If you have made all of your payments on time and never had a direct debit bounce, this heavily improves your chances of being approved.

2. Age of the Loan (The Principal Balance)

A refinance usually only makes sense for the lender (and for you) if you have repaid a reasonable amount of the original principal first.

If you borrowed $2,500 last month, it makes very little sense to refinance it today.

Lenders usually require a certain percentage of the loan to be paid down before they will entertain an internal refinance.

3. Standard Credit Assessment (Bank Statements)

Even though you are an existing customer, creating a new cash loan contract legally requires a brand-new credit assessment.

The lender will review your bank statements to ensure you are able to support the loan repayments, and that all other creit criteria is satisfied.

Benefits of Staying With Your Current Lender

Topping Up Your Cash (Borrowing More)

The most common reason people refinance internally with a cash lender is to borrow extra money.

Let’s say you took out a $2,500 MACC loan and have successfully paid it down to just $800. Suddenly, your fridge breaks, and you need $1,500 to replace it.

Instead of taking out a second loan, your current lender can refinance you so that you retain a single loan repayment.

They will close the $800 loan, open a new contract, and deposit the difference directly into your bank account.

Because they already have your details on file, this process is usually incredibly fast.

Extending the Loan Term to Lower Repayments

If you have had a sudden change in your financial circumstances and need to free up weekly cash flow, you could refinance to extend the term of your loan.

For example, if you have 6 months left in your loan, your lender might agree to refinance that remaining balance across a new 24-month term.

This will drop your monthly repayment significantly, giving your budget breathing room.

Just remember: stretching a loan over a longer period means you will pay more total interest and moving to a new loan would also trigger establishment fees that can be costly.

If your change in circumstances is temporary then contact your lender before attempting to refinance.

You may be able to lower or pause your repayments until the situation resolves itself.

Potentially Avoid Exit Fees

One of the biggest obstacles to external refinancing is the break fees that competitor lenders charge to close your loan early.

If you refinance internally, some lenders may be willing to waive their early exit fees to keep your business.

Note: If you are already with Gusto Cash, you don’t have to worry about this, as we never charge early repayment fees regardless of where you go!

The Cost Warning (Establishment Fees)

When you refinance a MACC personal loan, you are legally closing an old contract and opening a new one.

This means the lender will charge a brand-new establishment fee (capped at $400) on the new contract.

Because of this fee, you should only refinance if you genuinely need the additional funds.

Howvere, the same fee would be incurred if applying for a new MACC loan elsewhere so you may be no worse off sticking with the same lender as long as you can access the required funds.

Frequently Asked Questions

Is a refinance considered a brand-new cash loan?

Yes. Legally, the old MACC contract is paid out and closed completely. You will then sign a new contract with new terms, a new establishment fee, and a new repayment schedule.

Will refinancing with my current lender hurt my credit score?

Because an internal refinance is a new credit contract, the lender is required by law to conduct a new hard credit enquiry on your file. This can cause a small, temporary dip in your credit score, just as an external application would.

How much of my current loan do I need to pay off before I can refinance?

This depends entirely on the lender’s internal policies. Generally, most cash lenders prefer to see at least 25% to 50% of the original principal paid down with a perfect repayment history before they will approve a refinance.

Should You Stay or Switch?

Refinancing a personal cash loan with the same lender is a highly common and effective strategy if you need emergency funds or need to lower your repayments quickly.

A good repayment history with your current lender is your strongest asset for getting a fast approval.

However, you must always factor in the cost of the new establishment fee.

If your current lender charges an early repayment fee as part of the process then it may be time to shop around!

If you are looking for a transparent MACC loan between $2,001 and $5,000, or you want to switch to a lender that doesn’t punish you with early exit fees, the team at Gusto Cash is ready to help.