To qualify as a Medium Amount Credit Contract (MACC) personal loan, the repayment term must be between 16 days up to a maximum of two years.

While it may sound optimal to repay the loan in the shortest possible timeframe to get out of debt quickly, there is significant variation in the size of your repayments depending on the term you choose.

As a result, the size of the loan you can comfortably manage will also vary significantly.

In this article, we will walk you through the trade-offs between loan lengths, how your term affects your budget, and how to determine the best timeline for your personal loan.

Total Loan Cost vs Repayment Size

The two major variables to consider when selecting a loan term are the impact on your household budget (your repayment amount) and the total cost of credit (how much interest you pay overall).

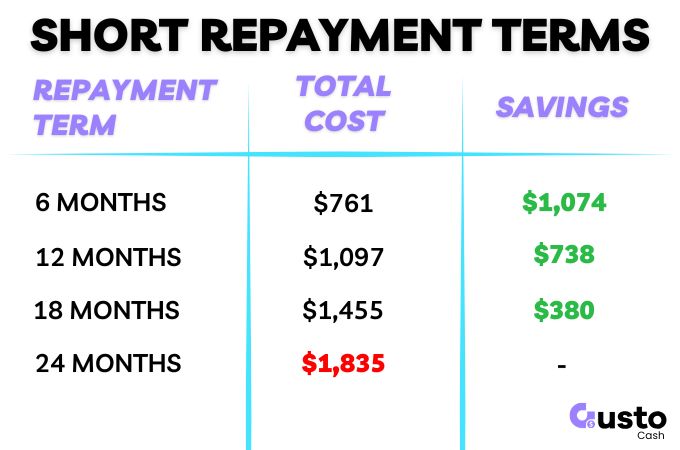

To demonstrate how the term impacts both, let’s look at a standard $2,500 MACC loan across two repayment scenarios.

In this example, you receive $2,100 directly into your bank account, and a standard $400 establishment fee is capitalised (added) to the loan, bringing the total starting balance to $2,500.

We will calculate the interest at the MACC maximum rate of 48% p.a (learn more about the Gusto Cash pricing structure on our costs page).

| Loan Feature | 6-Month Term | 24-Month Term |

| Cash Disbursed to You | $2,100 | $2,100 |

| Establishment Fee | $400 | $400 |

| Total Loan Principal | $2,500 | $2,500 |

| Estimated Monthly Repayment | ~$477 | ~$164 |

| Total Interest Charged | ~$361 | ~$1,435 |

| Total Amount Repaid | $2,861 | $3,935 |

| Total Cost of Finance | $761 | $1,835 |

The 6-Month Term

You get out of debt quickly and save over $1,000 in interest compared to the maximum repayment term!

However, the monthly repayments are almost three times the size.

This is the best outcome if you can comfortably manage the larger commitment from your household budget.

The 24-Month Term

The $164 monthly payment is far more flexible and easier to absorb into a normal household budget.

The trade-off is the increased total cost; you pay $1,435 in interest over two years for the convenience of the lower payments.

Neither option is universally better. The right choice depends entirely on your disposable income and your financial priorities.

Factors That Will Limit Your Loan Term

While you might want to choose your exact terms, there are factors on both the borrower and the lender’s side that will impose hard limits on your options.

1. Your Requirements & Objectives

What do you need the money for, and how quickly do you want to be debt-free?

If you are borrowing to cover a temporary cash flow gap, a short 3 to 6-month term makes sense.

If you are consolidating other scattered debts, stretching it out to 12 or 24 months might provide the breathing room you need to get on top of your finances.

As long as you are aware of the additional cost of doing so.

2. How Much You Can Afford

Lenders have a legal obligation to ensure a loan does not cause you substantial hardship.

If you apply for a $4,000 loan but your bank statements show you only have $200 of disposable income each month, a lender cannot approve you for a 6-month term.

You may be limited to a longer term where the payments fit your budget.

You then need to determine if this still meets your requirements and objectives mentioned in the previous point before accepting the offer of a longer term.

3. Lender’s Product Range

Under Australian consumer law, MACC personal loans are strictly capped at a 24-month maximum repayment term.

You cannot stretch a MACC loan over 3 or 5 years like you can with a car loan or a traditional bank loan.

If this is a requirement of yours then you should seek alternative finance.

4. Your Credit History

The longer the loan term, the higher the chance of your financial circumstances changing.

Lenders view longer terms as slightly riskier.

If you have a poor credit history or past defaults, a lender may restrict you to a lower borrowing amount and a shorter loan term to minimise their risk.

Frequently Asked Questions

Can I change my loan term after my contract has started?

Once your loan contract is signed and funded, the official term is locked in. However, you can effectively shorten your term at any time by making extra voluntary repayments on top of your scheduled direct debits, which pays down your principal faster.

Are there penalties if I choose a 24-month term but pay it off in 6 months?

At Gusto Cash, there are absolutely no early exit fees or penalties. Choosing a 24-month term to keep your mandatory minimum payments low, but paying extra whenever you have spare cash, is a fantastic strategy to protect your budget while still saving on interest. Some lenders will charge a fee for early repayment so you should check your loan contract prior to doing so.

Does picking a longer loan term guarantee I will be approved?

No. While a longer term lowers your monthly repayment and improves your basic serviceability calculations, your application will still be comprehensively assessed on your credit history, employment stability, and banking conduct.

How to Determine the Best Cash Loan Term for You

The math is simple, but the decision is personal.

To find the right balance, you should either:

- Determine exactly what you need to borrow, then calculate the shortest time period you can comfortably afford to repay it without putting yourself in any financial stress.

- Calculate your maximum safe monthly repayment amount from your household budget, and use this to determine what size loan you can afford over 12 or 24 months.

If you expect your situation to improve over time (e.g., you are starting a higher-paying job), you can safely start with the longest repayment term available to you to protect your current budget, and simply make additional, fee-free repayments as your income increases.

Remember that Gusto Cash does not charge any fees for early repayment of your MACC loan.

So you can make extra repayments as your circumstances allow to save money on the total cost of the loan. No matter what your original commitment was.

If you are ready to explore your borrowing power, the team at Gusto Cash is here to help you crunch the numbers.