The term Payday Loan has a stigma attached to it which is very real in terms of credit regulation and the damage it can do to someone’s finances.

However, in Australia, payday loans are so heavily regulated that consumers will not encounter the predatory practices that are possible elsewhere.

They are still more expensive than a regular personal loan. So why would one choose a payday loan over a personal loan?

The answer depends on the urgency of the need for cash, the borrower’s credit profile, and their intended pay back period.

In this article, we’ll discuss these reasons in detail and compare each loan product and who it is most suitable for.

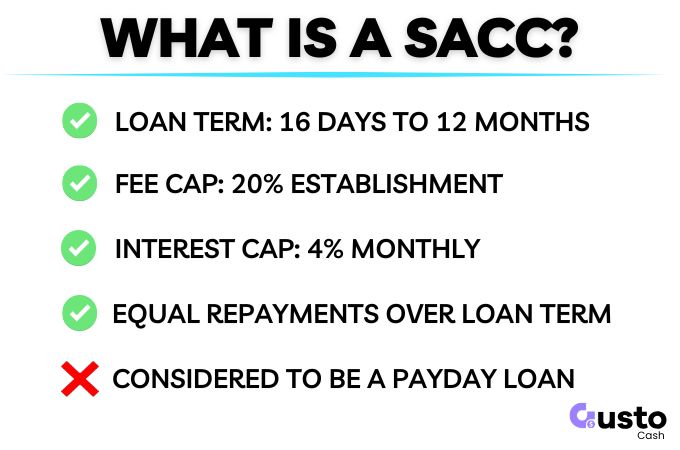

Australian Credit Contract Categories

There are three tiers of credit contracts available in Australia for borrowers that are relevant to a comparison of payday and personal loans.

Each with their own set of specific rules and consumer protections that place hard limits on cost, eligibility, and the required checks before approving a loan.

- A Small Amount Credit Contract (SACC) is short term, high cost, and broadly accepted as a payday loan.

- A Medium Amount Credit Contract (MACC) is usually positioned as a cash loan or medium loan.

- A Personal Loan is a broader consumer loan category offered by mainstream lenders with larger loan amounts and longer repayment terms.

A SACC loan is the modern equivalent of a payday loan in Australia.

Whereas a MACC can be repaid over a longer period of time to reduce the pressure on your budget while you get back on top.

Gusto Cash only offers MACC loans which are lower cost and can have more favourable loan terms than a SACC (Payday Loan).

Click below to start your application today.

Payday Loans vs Personal Loans Comparison

Generally speaking, a payday loan serves a specific purpose when there is an urgent need for cash and there is no other alternative.

It is important that you can afford to repay the loan as quickly as possible so that you can minimise the cost incurred.

A personal loan is a broader product that can be used for almost any major purchase, and is priced in ways to suit mainstream borrowers.

Summary Table

| Loan Parameters | Payday Loan | Personal Loan |

| Loan Amount | Up to $2,000 | $5,000 to $100,000+ |

| Loan Term | 16 days to 12 months | 3 to 7 years |

| Establishment Fee | 20% of loan amount | $0 to $1,000 |

| Ongoing Cost | 4% monthly fee (based on loan amount) | ~5% to 30%+ interest rate |

| Approval Timeframe | 0-2 days | 0-7 days |

| Security | Unsecured | Secured or Unsecured |

| Max. Repayment Amount | 10% of income | NA |

| Max. Recent Loans | 2 or more in 90 days | NA |

1. Speed to Approval

Personal loans have traditionally been much slower to approve and fund.

But this is changing with a range of modern non-bank lenders offering fast turnarounds and very competitive rates.

If you go to a bank though you are likely still going to be waiting a while before final approval is given (if at all).

Whereas a payday loan is designed to be fast and usually funded the same day as the application, if approved.

This is the main benefit of a short term cash loan and is great for dealing with time sensitive expenses.

2. Loan Amount

The amount of credit available under each type of loan contract is strictly regulated to the following bandings:

- SACC: $2,000 or less.

- MACC: $2,001 to $5,000.

- Personal Loan: $5,000 or more.

So if you only want to borrow $1,000 your only option is a payday loan contract.

For a larger purchase, like a car, you will only be able to fund it with a personal loan (unless it is a very cheap car!).

3. Cost of Funds

This is where the loan categories really diverge and there are multiple reasons for this, including:

- Short term loans accumulate less interest and need a higher rate to generate the dollar return for a lender.

- Lower balances also accumulate less interest/fees.

- The cost incurred by the lender to write a loan is similar whether the loan is $1,000 or $50,000.

The cost structures are strictly controlled for a payday loan.

Whereas a personal loan is set more by market forces,but still subject to legal maximum Annual Percentage Rate (48%).

- Payday loans: 20% upfront establishment fee and a maximum 4% monthly fee based on the borrowed amount.

- Personal loans: Establishment fee set by the lender, and an interest rate also set by the lender (from ~6% up to 30%+).

You will see personal loans advertised at interest rates around the 6% mark, which sounds amazing!

However, these are often restricted to customers with a very high credit score (800+) and may also need to be a property owner.

Lower credit scores may get pushed into an interest rate exceeding 20% for an unsecured personal loan.

Establishment fees will also vary depending on the type of personal loan and can range from $0 up to $1,000.

4. Loan Term

A payday loan has a minimum loan term of 16 days and up to12 months.

Given the higher cost nature of this product the shorter the repayment period the better for the borrower.

A personal loan is typically repaid over a longer timeframe that ranges from three to seven years.

This allows for much higher loan amounts.

For example, a $100,000 secured car loan requires a longer repayment period so that the installments are affordable.

5. Credit Profiles and Eligibility

All consumer lending in Australia is subject to strict responsible lending obligations designed to protect consumers from unmanageable debt.

Lenders must assess your financial situation to ensure ongoing repayments will not cause substantial financial hardship.

This is true for all types of loans, including personal loans, mortgages and car loans.

However, a SACC loan is subject to a much stricter set of requirements.

Two points that must be included in the credit assessment prior to the provision of credit are as follows:

- Protected earnings: SACC repayments cannot exceed 10% of your income.

- Multiple SACC Loans: A borrower is deemed unsuitable if they have had two or more SACC loans in the past 90 days.

A personal loan or a MACC is not subject to these conditions.

These rules are designed to provide additional protection to vulnerable borrowers who are more likely to resort to SACC loans, and end up in a risky debt position.

Personal loans eligibility starts with your credit score which determines how your loan will be priced.

If you have a strong credit history you should be eligible for a much cheaper rate than someone who has blemishes on their credit report.

Once you fall below a certain point you will no longer be eligible for mainstream credit products such as a personal loan.

However, you may still be able to get a payday loan or a MACC in some circumstances if you are recovering from bad credit events.

6. Impact on Future Credit Eligibility

It is common for lenders to have specific exclusions in their credit policy for those who regularly engaged with payday loans.

Even sub-prime lenders who specialise in credit impaired consumers may immediately reject a loan application if more than two or three SACCs are evident within a set period of time.

Other SACC lenders are obligated to reject your application if you are a regular SACC borrower if you hit the regulatory limit.

So the bottom line is that it is not good for your future credit prospects.

A personal loan application may lead to a short term hit to your credit score, but that will be the case for most credit products.

The score will also rebound quickly afterwards in the absence of further applications or any missed payments.

So there are no ongoing considerations for credit eligibility with a personal loan as long as you meet all of your obligations.

The only change will be your capacity to service future debt will be reduced for as long as you are making payments on your personal loan.

Who is Best Suited to a Payday Loan or Personal Loan?

The right loan choice is generally determined by the amount you need, your ideal timeframe to repay the loan, and your credit score.

Payday Loans are Most Suitable For

- Credit impaired borrowers who cannot access mainstream alternatives like a credit card or personal loan.

- Borrowers who need less than $2,000 and can repay the loan within a shorter timeframe.

- Small, urgent bills, where there is no hardship program available or you do not qualify.

Personal Loans are Most Suitable For

- Those with a mid to high credit score who require a larger loan.

- Larger purchases or cash needs where repayments can be sustained over years.

- Can tolerate a longer approval period before the loan is funded.

A MACC loan can also bridge the gap for those needing between $2,001 and $5,000, and still need an urgent resolution to their cash needs.

Frequently Asked Questions

What is the difference between personal and payday loans?

Payday loans (SACCs) are capped at $2,000 with higher fixed fees and rapid repayments. Personal loans offer larger amounts and longer terms with standard interest rates.

Is a MACC a payday loan?

No. A Medium Amount Credit Contract (MACC) strictly covers loans between $2,001 and $5,000. It provides structured terms and capped fees, and longer repayment periods.

Which is best if I need money today?

Both MACCs and payday loans fund quickly, whereas bank loans can take days. However, the speed to receive the funds is only part of the assessment for whether a loan is the best for your circumstances.

Payday Loans as a Last Resort

If you can avoid using an expensive SACC loan then in most cases you will be better off looking elsewhere.

When you need access to quick cash, and have the means to repay comfortably, then it can be the best solution.

Gusto Cash offers MACC loans with high limits and longer potential repayment periods. If this is more suitable for your needs then click below to get started.