Short term cash lending is different from your standard personal loan, which is usually repaid over many years.

They are designed to fill a gap in your finances when you have an unexpected bill or large expenses that need to be paid quickly.

Think urgent car repairs, rental bonds, medical expenses. The type of bill that is time sensitive and relatively low amounts.

This type of loan is generally higher cost compared to a larger personal loan, but the shorter repayment period largely offsets that.

Which makes it an important tool when there is an urgent need for cash.

In this article, we will help you understand these two main categories of short term loans, who they are most suited to, and the cost involved.

Fast Cash Loan Categories

The two types of quick cash loans summarised below are based on specific legislated categories.

There are strict rules around who can offer these loans, the terms available, and the cost associated with this type of finance.

While Gusto Cash only offers a MACC loan product, the information below is objective and largely driven by government regulations.

To check your eligibility for a Gusto Cash Loan, click below.

What is a Small Amount Credit Contract (SACC)?

A SACC is a regulated short-term cash loan designed for urgent cash needs and a fast payback period.

Under Australian consumer law, SACCs operate within specific boundaries:

- Loan amount: Capped at a maximum of $2,000.

- Term length: Restricted to between 16 days and one year.

- Price structure: 20% upfront establishment fee and a maximum 4% monthly fee based on the borrowed amount.

While SACCs offer immediate cash, borrowers must carefully manage the costs.

The recurring 4% monthly charge means your total fees stack up fast over a longer repayment term.

Additionally, relying on these loans repeatedly to cover regular living costs will trap you in a stressful debt cycle.

They are best for small, short-lived financial emergencies where you can comfortably repay the balance fast.

What is a Medium Amount Credit Contract (MACC)?

A MACC can provide access to larger cash amounts for significant purchases, or one off expenses, that can be repaid over a slightly longer timeframe.

They are another highly regulated personal loan designed to offer medium-sized, predictable repayments.

Under Australian consumer law, the parameters are strictly limited to:

- Amount and term: Borrow between $2,001 and $5,000 for up to two years.

- Price structure: Lenders charge a capped establishment fee ($400) and an annual interest rate (48%).

These loans can be secured or unsecured, with some borrowers using the funds to buy a used car or other vehicle under $5,000 that can be used as security.

Other common uses for a MACC personal loan include:

- Consolidating scattered small debts.

- Paying rental bonds or moving costs.

- Covering larger vehicle repairs.

- Household repairs and appliance replacement.

MACCS can be most suitable for borrowers who need $2,000 to $5,000 and want a longer, predictable repayment schedule than is offered by a SACC.

SACC vs MACC: Detailed Comparison

We have compared each loan product based on five categories.

In most cases, your choice of product will be dictated by legislation rather than preference.

However, the comparison below will help you understand why so you can determine your objectives clearly before applying for credit.

Summary Table

| Loan Parameters | SACC | MACC |

|---|---|---|

| Loan Amount | Up to $2,000 | $2,001 to $5,000 |

| Loan Term | 16 days to 12 months | 16 days to 24 months |

| Establishment Fee | 20% of Loan Amount | Up to $400 |

| Ongoing Cost | 4% monthly fee (based on loan amount) | Up to 48% interest |

| Security | Unsecured Only | Secured or Unsecured |

| Max. Repayment Amount | 10% of income | NA |

| Max. Recent Loans | 2 or more in 90 days | NA |

1. Loan Amount

Each loan product can only be offered within a specific range for the loan amount.

$2,000 and below must be a SACC, and over $2,000 a MACC.

- Loan A: $2,000 SACC

- Loan B: $2,001 MACC

MACCs are capped at $5,000 and cannot be offered for a higher loan amount.

2. Loan Terms

The range of repayment terms are also restricted for both SACC loans and MACCs.

Both have a minimum of 16 days, but a variable maximum loan term.

- Loan A: $2,000 SACC, maximum loan term of 12 months.

- Loan B: $2,001 MACC, maximum loan term of 24 months.

A lender is not obligated to offer these maximum loan terms, but they cannot exceed them.

In the above scenarios, the MACC loan would have much lower repayments given the longer maximum term. However, the total cost of credit would also increase.

3. Costs

There are two main elements that make up the cost of these short term loan products; the establishment fee, and the interest cost.

Regulations dictate strict caps on both, with the terminology used for each contract type also slightly different.

Establishment Fees

This fee is added to the principal amount paid to you on the day the loan is funded.

So you will owe more than you receive regardless of the loan type.

The calculation method varies depending on the type of loan contract:

- SACC: up to 20% of loan amount

- MACC: up to $400

You may notice that the MACC becomes much cheaper relative to the loan amount the larger the loan is.

Compared to a SACC that is a fixed percentage that applies no matter the loan size.

Ongoing Cost

The ongoing cost of a loan is usually calculated based on an interest rate.

While this is the case for a MACC loan, a SACC loan has a different pricing structure.

A SACC lender can charge up to 4% of the loan amount for the duration of the repayment period.

This fee does not reduce as you repay the loan and stays fixed for every month the loan is open.

Whereas a MACC has a maximum annual interest rate of 48%.

While this sounds high, it is calculated on the outstanding balance that reduces quickly over the short repayment period.

As a result, a SACC loan is almost always more expensive relative to the amount borrowed.

SACC vs MACC Total Cost Example

We’ll continue with the same two loan examples to demonstrate the difference in the cost structures over the same repayment term (6 months).

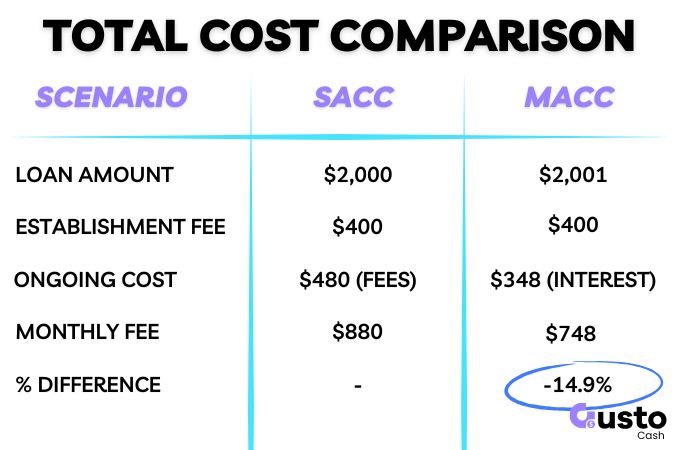

Example A: $2,000 SACC

- Establishment fee: $400 (20% of principal)

- Monthly fees: $480 (4% of $2,000 x 6 months)

- Total repayment: $2,880 (principal plus fees)

- Total cost: $880.00

Example B: $2,001 MACC

- Establishment fee: $400

- Annual interest: 48% p.a. calculated on a reducing balance

- Total repayment: $2,748.12

- Total cost: $748.12

The MACC loan is almost 15% cheaper than the SACC. The difference is largely due to the way the monthly fee is calculated.

For larger loan balances the cost of a MACC reduces further in relation to the loan amount.

The same $400 fee would be applied on a $5,000 loan (8% of loan amount) as a $2,001 loan (20% of loan amount).

Whereas a SACC is a fixed 20% of the loan amount.

4. Credit Accessibility

All consumer lending in Australia is subject to strict responsible lending obligations designed to protect consumers from unmanageable debt.

Lenders must assess your financial situation to ensure ongoing repayments will not cause substantial financial hardship.

This is true for all types of loans, including MACCs, mortgages and car loans.

However, a SACC loan is subject to a much stricter set of requirements.

Two points that must be included in the credit assessment prior to the provision of credit are as follows:

- Protected earnings: SACC repayments cannot exceed 10% of your income.

- Multiple SACC Loans: A borrower is deemed unsuitable if they have had two or more SACC loans in the past 90 days.

A MACC loan is not subject to these conditions.

These rules are designed to provide additional protection to vulnerable borrowers who are more likely to resort to SACC loans, and end up in a risky debt position.

5. Impact on Future Credit Applications

It is common for lenders to have specific exclusions in their credit policy for those who regularly engaged in SACC borrowing.

While not technically a payday loan, it is viewed as such by other lenders and is a high-risk indicator.

Even sub-prime lenders who specialise in credit impaired consumers may immediately reject a loan application if more than two or three SACCs are evident within a set period of time.

As discussed in the previous section, even other SACC lenders must reject your application if you are a regular SACC borrower if you hit the regulatory limit.

So the bottom line is that it is not good for your future credit prospects.

MACC loans do not have any specific regulatory thresholds to consider, and some lenders may be more forgiving than others.

However, repeatedly using short-term credit can be a signal of cash flow stress and not something a mortgage lender would view favourably, for example.

Who is Best Suited to a SACC or MACC?

The right loan choice is generally determined by the amount you need, and your ideal timeframe to repay the loan.

There is limited overlap on these two points which reduces the scope for consumer choice between a MACC and SACC.

SACCs are Most Suitable For

- Credit impaired borrowers who cannot access mainstream alternatives like a credit card or personal loan.

- Borrowers who need less than $2,000 and can repay the loan within a shorter timeframe.

- Small, urgent bills, where there is no hardship program available or you do not qualify.

MACCs are Most Suitable For

- Credit impaired borrowers who cannot access mainstream alternatives like a credit card or personal loan.

- Borrowers who need $2,001 to $5,000 and want structured repayments over a longer timeframe.

- Borrowers who are purchasing an asset that could be used as security over the loan to improve the chance of being approved.

Alternatives Options For Vulnerable Consumers

The regulations around SACCs and MACCs are intended to prevent vulnerable consumers from being stuck in a debt situation they cannot resolve.

But access to credit can also be a critical need for this group.

For anyone experiencing financial hardship, and needs access to credit, they should explore these alternative programs:

- No Interest Loan Scheme (NILS): Zero-interest funding for essential goods.

- Government support: Centrelink advance payment if you receive eligible benefits.

- Hardship plans: Negotiate a payment plan directly with your utility provider.

Frequently Asked Questions

What are the main cost differences between a SACC and a MACC?

Both loans have an establishment fee and ongoing costs. A SACC charges an establishment fee up to 20% of the loan amount plus an ongoing monthly fee of up to 4%. A MACC charges an establishment fee capped at $400, along with a maximum annual interest rate of 48% calculated on a reducing balance, which typically makes it cheaper relative to the borrowed amount.

Who is a SACC loan most suitable for?

A SACC loan is generally most suitable for borrowers with impaired credit who cannot access mainstream financing and need to borrow less than $2,000 for small, urgent bills or emergencies where hardship programs are unavailable, provided they can comfortably repay the amount within a short timeframe.

Who is a MACC loan most suitable for?

A MACC is most suitable for borrowers who are seeking a loan amount between $2,001 and $5,000, and prefer a structured, predictable repayment plan over a longer timeframe (up to 2 years) compared to a SACC.

Does Gusto Cash offer both SACC and MACC loans?

No, Gusto Cash exclusively offers MACC loan products.

Is a SACC or MACC Loan Best?

The cost of a MACC will always be lower in relation to the amount of credit due to the fixed establishment fee and interest rate charged on the outstanding balance.

There are also fewer restrictions on who can obtain a MACC within the Australian credit regulations.

You also have the option to repay the loan in a shorter timeframe that is comparable with a SACC.

However, a larger loan amount is required to qualify and there is no flexibility on this.

SACC loans can be suitable for those who are within the regulated criteria and are able repay the loan in less than 12 months.

If you are in the market for a MACC loan then click below to check your eligibility with the team at Gusto Cash.